07/2020: Stability of Prices for Disability Insurance

This special research deals with the expected stability of your premiums for disability insurance products.

In the current environment of low interest rates, life insurers must first and foremost earn the guaranteed interest for life insurance products. If the returns on the capital market are not sufficient, there is a risk that returns from the term life products will be used to finance life products. Such cross-financing between different products and sources of profit is permissible under supervisory law and is also fully in line with the insurer’s collective approach. However, in this case the term life products receive less surplus and the premiums to be paid increase. This potentially affects term life insurances, and especially disability insurance products.

We want to inform which life insurers are strong enough.

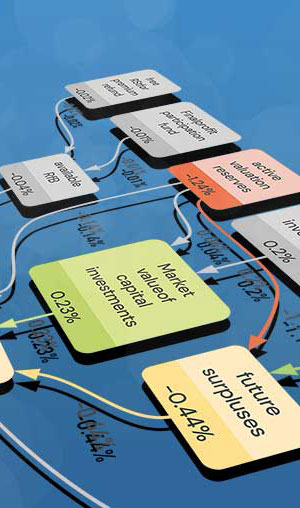

These probably do not have to reduce the surplus participation for risk products or increase their premium payments. To this end, we have looked at what return remains from profit participation of technical returs after insufficient capital market returns have been financed from these funds. In our analysis we assumed a very tough scenario of permanently low interest rates. As a result, in particular those life insurers perform well having high technical profits on the one hand and no holes to plug caused by low capital market returns for traditional products on the other.

As a key figure we have developed the technical net interest rate.

The higher this earned interest rate is, the less likely it is that premiums will increase due to low interest rates. As a result, we see that the situation varies greatly from one disability insurance provider to another.

Deutsche Ärzteversicherung and Neue Bayerische Beamten Leben have the strongest starting position for high and stable premiums in the future for term and disability insurance. Both insurers have a very strong technical net interest rate of over 3%. Strong insurers follow in 3rd to 10th place with a technical net interest rate of 1% to 2%. The strong insurers in particular have enough potential to pass on risk profits to customers undiminished – even in times of very low investment income.

In a series of interviews, Holger Bartel from the independent rating agency RealRate answers questions about disability insurance and the RealRate survey. All for the benefit of customers, because financial strength secures its future surplus participation:

Part 1: What should be considered from the customer’s point of view with regard to disability insurance? What role does profit participation play?

Part 2: Why is it important to pay attention to the financial strength of providers of disability insurance? Why are disability customers also affected by low interest rates?

Part 3: The RealRate approach to rating insurance companies: Financial strength is brought to the fore. Using modern artificial intelligence methods, the causes of financial strength are analyzed and explained.